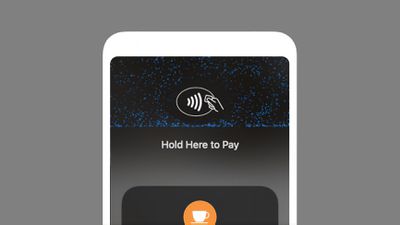

The second beta of iOS 15.4 adds code for the new "Tap to Pay" feature that Apple announced this morning. "Tap to Pay on iPhone" is designed to allow NFC-compatible iPhones to accept payments through Apple Pay, contactless credit and debit cards, and other digital wallets, without requiring additional hardware.

Tap to Pay on iPhone is enabled in the latest beta, but it does require third-party providers to add support, so it is not yet available for use. There are no outward-facing signs of it that are visible to end users, but there's a new "PaymentReceived" sound file and images that show off the Tap to Pay interface.

MacRumors contributor Steve Moser has also discovered references to a "ContactlessReaderUIService" in the code, as well as mentions of alerts that end users will see. The feature will support reward passes and refunds.

- iPhone ready to accept a contactless payment.

- Hold your card or device to the seller's iPhone and wait for the success sound.

- To accept contactless payments, turn on NFC and try again.

- The payment timed out for your security. Try again when you are ready to accept a payment.

- Multiple reward passes applied

- Pay %@ %@

- Refund from %@ for %@"

- Try Again & Hold Card Longer

- Use your iPhone to accept payments from contactless credit and debit cards, Apple Pay, or any other contactless payment devices.

The Tap to Pay feature will work with the iPhone XS or later, and will allow supported iOS apps to accept iPhone to iPhone payments. At checkout, a merchant is able to prompt a customer to hold their iPhone, Apple Watch, contactless credit or debit card, or other digital wallet close to the merchant's iPhone to complete a payment over NFC.

Stripe has announced that it will be the first payment platform to offer Tap to Pay on iPhone to business customers, including Shopify users, later this spring. Apple Stores in the U.S. will also roll out support for the feature later this year.